Actively Managed Equity

Actively Managed Equity Overview: All Strategies

Overview: All Strategies Investor Resources

Investor Resources Indexed Equity

Indexed Equity Private Equity

Private Equity Digital Assets

Digital Assets Invest In The Future Today

Invest In The Future Today

Take Advantage Of Market Inefficiencies

Take Advantage Of Market Inefficiencies

Make The World A Better Place

Make The World A Better Place

Articles

Articles Podcasts

Podcasts White Papers

White Papers Newsletters

Newsletters Videos

Videos Big Ideas 2024

Big Ideas 2024

Auto Sales will Fall in a Vibrant Sharing Economy

While auto sales have been one of the most important gauges of economic well being historically, the sharing economy could strip them of that role during the next five years. Thanks to web-enabled services like Zipcar [CAR], Uber, Lyft, and Flightcar, household vehicles are beginning to feel like the stranded assets they are: high in cost, but utilized only 4% of the time on average in a 24-hour day. Based on various studies,[1] sharing services could increase vehicle utilization by eight- to twelve-fold,[2][3][4] activating stranded assets and boosting the efficiency of the U.S. capital base.

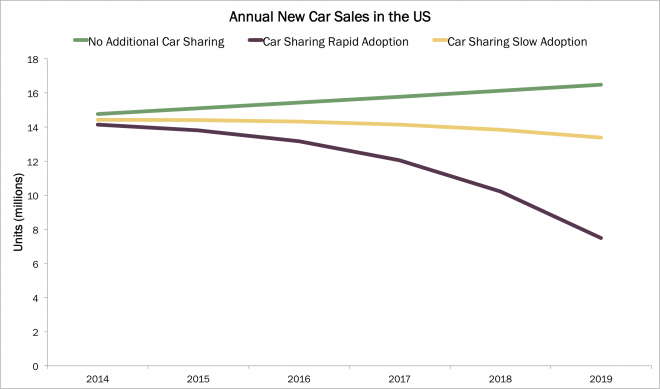

“Transportation-as-a-service” looms as a significant challenge to the auto sector. Many individuals, who typically would buy cars after landing their first jobs, or two cars after moving to the suburbs, are rethinking the economics of those decisions given the burst in alternative means of transportation with the rise of a sharing economy. As the graph below illustrates, if the U.S. economy were to continue expanding during the next five years, and sharing services were to increase to 2.5-5% of all household car rides, auto sales would decline. At 2.5% penetration, the drop would be slight but, at 5%, auto sales would collapse from 15.6 million units in 2013 to 7-8 million units…and that would be in a good economy!

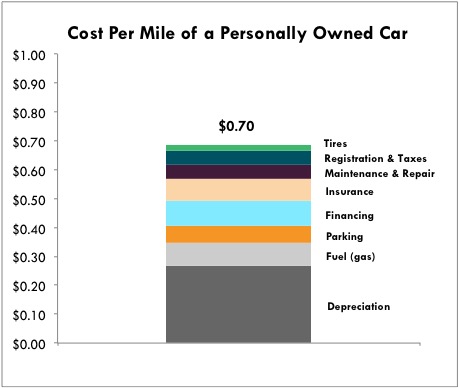

Shared autonomous vehicles (SAVs) could push this trend into overdrive, especially if Google [GOOG] delivers on its promise of a fully autonomous vehicle during the next five or six years, regulation permitting. As is illustrated below, the current cost to own and operate a personal car is $0.70 per mile driven, including depreciation, gas, parking, financing, insurance, maintenance, registration, taxes and tire replacement. For many people, parking and speeding tickets add regularly to these costs.

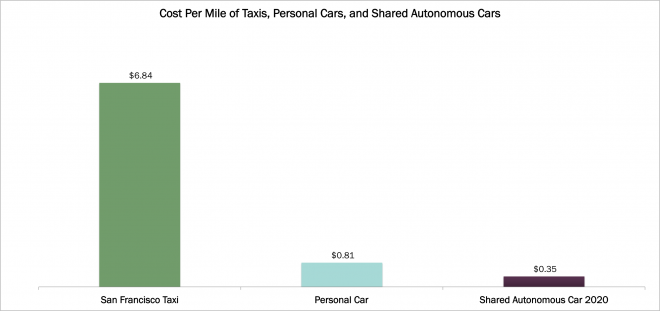

While SAVs still have at least a few years of technological and regulatory hurdles to jump, if they were on the road today they would be cost competitive with personal vehicles, thanks to much higher utilization rates, and far less expensive than taxis, as shown in the graph above. When they do hit the road, SAVs will become more compelling over time given their high technology content and the declining cost curves which typify technology. By the end of the decade, costs could be cut in half to $0.35 per mile.

Yet, cost is just one of the benefits of shared autonomous vehicles. Others, such as safety, convenience, and discretionary time, would cement the case for SAVs were they permitted on the roads today. Safety is the most serious of these considerations. Human error contributes to 90% of all auto accidents in the United States today. Consequently, U.S. regulators may be swayed sooner than most analysts believe by arguments that autonomous vehicles could prevent nearly 30,000 deaths per year. The value proposition here is clear, and it will become clearer as regulators pave the way and SAV costs decline.

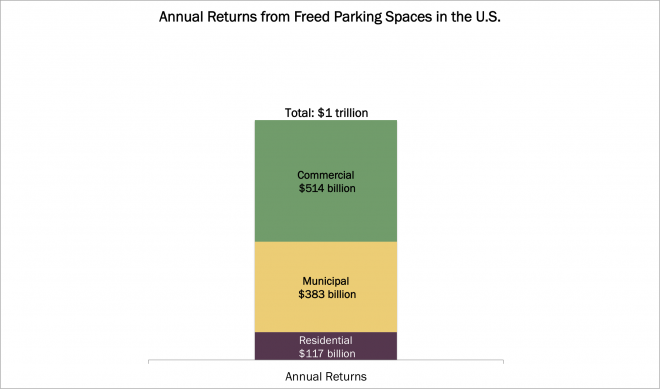

Shared Autonomous Vehicles will Free Residential, Commercial and Municipal Real Estate for Higher Returns

Parking lots occupy a lot of otherwise productive space around the world, a problem that SAVs will solve in large part. Spending eight- to twelve-fold more time on the road than traditional cars, SAVs would require only one parking space in reserve per car, compared to the five in place today.

If SAVs were to replace 60% of the personal vehicles in the U.S., they would free up roughly 740 million parking spaces worth $13 trillion at today’s values, more than 85% accruing to commercial real estate owners and municipalities. Repurposing the land and buildings would deliver significant incremental returns on invested capital. In a vibrant sharing economy, homeowners could turn garages into rooms or larger yards, while commercial real estate owners might build out more offices, retail storefronts, or apartments. Municipalities will lose parking fees but could sell off their parking lots to compensate, ultimately turning parking fees into real estate taxes. By our estimates, converting parking lots would add roughly $1 trillion, or 7.7%, per year to homeowner, commercial, and municipal real estate returns.

[av_button label=’Download Free White Paper’ link=’manually,http://research.ark-invest.com/new-markets-new-metrics’ link_target=’_blank’ color=’theme-color’ custom_bg=’#444444′ custom_font=’#ffffff’ size=’large’ position=’left’ icon_select=’no’ icon=’ue800′ font=’entypo-fontello’ av_uid=’av-37a2pt’]

This article is part of a series based on Disruptive Innovation: New Markets, New Metrics, a compelling white paper written by ARK Investment Management in collaboration with Dr. Arthur Laffer (Laffer Associates, LLC).